Excellent Strong Suggestions Regarding Residence Mortgages That Anybody Can Use

Content written by-Drachmann ThompsonIt isn't impossible to get an amazing mortgage - one you can afford which offers the amount of money you need to buy or renovate your home - but it does take effort. The first step is to do your research, learning about mortgages. The tips below will make that job easy, so dive right in!

Work with your bank to become pre-approved. Pre-approval helps give you an understanding of how much home you can really afford. It'll keep you from wasting time looking at houses that are simply outside of your range. It'll also protect you from overspending and putting yourself in a position where foreclosure could be in your future.

Understand your credit score and how that affects your chances for a mortgage loan. Most lenders require a certain credit level, and if you fall below, you are going to have a tougher time getting a mortgage loan with reasonable rates. A good idea is for you to try to improve your credit before you apply for mortgage loan.

Have all your ducks in a row before walking into a lender's office. In the event that you arrive without sufficient documentation of your current earnings and other relevant information, you may quickly be dismissed, and asked to return when you do have everything in hand. The lender is going to want to go over all this information, so getting it together for them can save time.

You may be able to add your homeowners insurance costs to your mortgage payment. One advantage of this is negating the need to make two payments. Instead of paying your mortgage and an insurance bill, you can pay both bills in one payment. If you like to consolidate your bills, this is a good idea.

It is likely that your mortgage lender will require a down payment. In the past, home owners often had the ability to get a loan without having to offer a down payment up front. That is mostly not the case anymore. Ask what the down payment has to be before you send in your application.

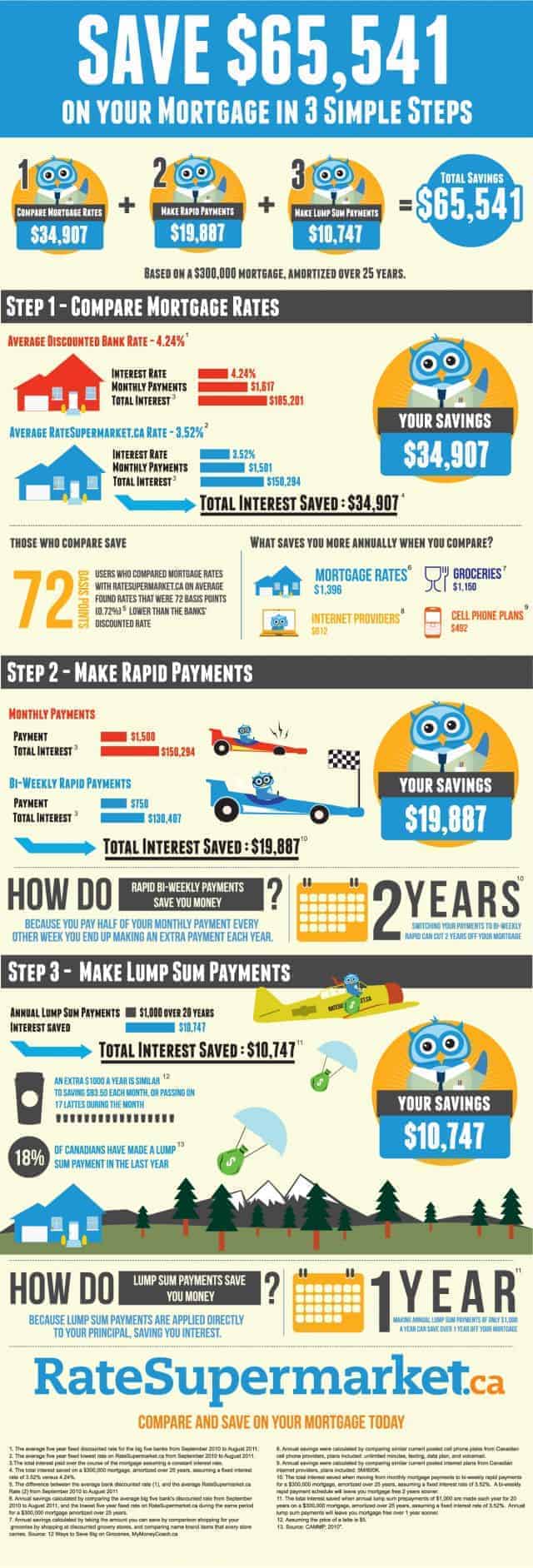

If you are able to pay more for your monthly payments, it is a good idea to get a shorter-term loan. Most lenders will give you a lower rate if you opt to pay your mortgage over 20 years instead of 30 years. Borrowers who get shorter term loans (such as 15 or 20 years terms) are considered less risky than those with longer term loans, resulting in lower interest rates.

Getting the right mortgage for your needs is not just a matter of comparing mortgage interest rates. When looking at offers from different lending institutions you must also consider fees, points and closing costs. Compare all of these factors from at least three different lenders before you decide which mortgage is best for you.

Don't apply for new credit and don't cancel existing credit cards in the six months before applying for a mortgage loan. Mortgage brokers are looking for consistency. Any time you apply for credit, it goes on your credit report. Avoid charging a large amount during that time and make every payment on time.

Make sure you're not looking at any penalties when you apply for a new mortgage. Your old mortgage may impose fines for early payment, which can include refinancing. If there are fines, weigh the pros and cons before getting into a new mortgage, as you may end up paying a lot more than you expected, even though refinancing means a lower monthly payment.

A mortgage broker can be a good alternative if you are finding it hard to get a mortgage loan from a credit union or regular bank. Many brokers can find mortgages that fit your situation better than these traditional lender can. They work with different lenders to get the best option for you.

Be wary of mortgage lenders who promise you the moon. Most lenders work on commission. So, it goes without saying that there are dishonest lenders who will promise anything to get a commission. Remember that you can back out of loan application at any time if you do not feel comfortable.

Before you contact a mortgage lender to apply for a loan to buy a home, use one of the fast and easy mortgage calculators available online. You can enter your loan amount, the interest rate and the length of the loan. The calculator will figure the monthly payment that you can expect.

Having a pre-approval letter from your lender will let sellers know you are serious about buying a home. There will be no doubt about whether or not you can buy a home. The approval letter should be the amount of the offer you make. If the amount in the letter is greater than your offer, it will tip the seller off.

Remember that it takes time to get a mortgage closed; therefore, it is important to include enough time in the sales contract for the loan to close. Although it may be tempting to say the deal will be closed within 30 days, it is best to use a 60 or 90 day timeframe.

Opt out of credit offers before applying for a home mortgage. Many times creditors will pull a credit file without your knowledge. This can result in an immediate decline for a home mortgage. To help prevent this from happening to you, opt out of all credit offers at least six months before applying for a loan.

After you receive a loan approval, you may stop paying close attention. But avoid making https://www.nerdwallet.com/article/small-business/what-you-need-to-open-a-business-bank-account that will change your credit rating at this time. An approval is not the end to credit monitoring for you, as the lender will be attuned to changes. If you were to take on a higher credit card balance, or a new auto loan, they can take back their offer.

Don't believe all the promises made by certain mortgage lenders. There are often a lot of marketing shenanigans going on with big promises. There's often a lot hidden right below the surface, and it's never anything good for you. Look for a lender who is realistic and sincere in its dealings with you.

Never choose a home mortgage from a company that asks you to do unscrupulous things. If a rep is asking you to claim more than you make to secure the mortgage, it's not a good sign that your mortgage is in good hands. Walk away from these deals as quickly as you can.

With the advice that has been given to you, you are now equipped to enter the mortgage market and begin deciding which route you want to take. It's important that you understand all of your options, and you want to feel in control and not thrown into a mortgage by a lender that doesn't fit your needs. Instead, go forth and get the right mortgage!